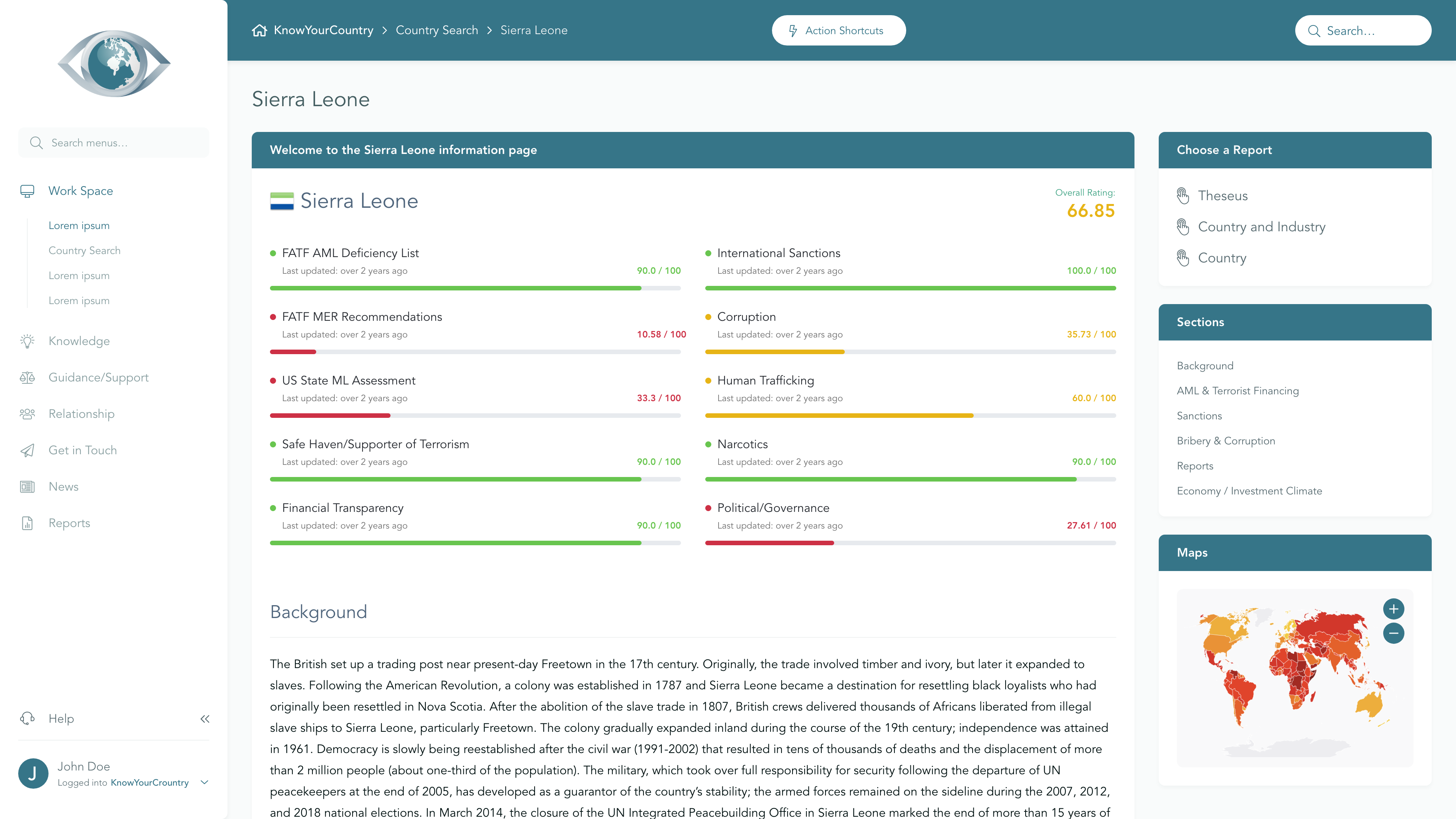

Russian Federation Country Summary

Higher Risk

View full Ratings TableSanctions

Higher Concern

FATF AML Deficient List

Higher Concern

Terrorism

Medium Concern

Corruption

Higher Concern

US State ML Assessment

Higher Concern

Criminal Markets (GI Index)

Higher Concern

EU Tax Blacklist

Higher Concern

Offshore Finance Center

Lower Concern

Please note that although the below Summary will give a general outline of the AML risks associated with the jurisdiction, if you are a Regulated entity then you may need to demonstrate that your Jurisdictional AML risk assessment has included a full assessment of the risk elements that have been identified as underpinning overall Country AML risk. To satisfy these requirements, we would recommend that you use our Subscription area.

If you would like a demo of our Subscription area, please reserve a day/time that suits you best using this link, or you may Contact Us for further information.

Anti Money Laundering

FATF Status

The Russian Federation is not on the FATF List of Countries that have been identified as having strategic AML deficiencies. However, FATF has suspended the FATF membership of the Russian Federation due to its invasion of Ukraine.

Compliance with FATF Recommendations

The last Mutual Evaluation Report relating to the implementation of anti-money laundering and counter-terrorist financing standards in Russia was undertaken in 2024. According to that Evaluation, Russia was deemed Compliant for 6 and Largely Compliant for 31 of the FATF 40 Recommendations. It remains Highly Effective for 2 and Substantially Effective for 4 with regard to the 11 areas of Effectiveness of its AML/CFT Regime.

Sanctions

The report details a broad, coordinated sanctions regime enforced against Russia by multiple nations and regions, including the United States, the European Union, the United Kingdom, Canada, Australia, Japan, New Zealand, and Switzerland, with additional autonomous measures by other allies, targeting asset freezes, export controls, financial sector restrictions, and bans on energy and dual-use goods, along with oil price caps and shadow fleet designations. As of 2025, these measures amount to thousands of individual designations (e.g., over 16,000 in the United States and more than 2,400 in the European Union) and comprehensive restrictions across imports, exports, finance, and maritime services, while some regions—most notably the Arab League—have not imposed collective sanctions.

Criminality

Rating |

0 (bad) - 100 (good) |

|---|---|

| Transparency International Corruption Index | 22 |

| World Bank: Control of Corruption Percentile Rank | 16 |

The state of crime and corruption in the Russian Federation remains deeply entrenched, with high levels of corruption affecting various sectors, particularly public procurement and law enforcement. Despite some government initiatives aimed at combating corruption, such as increased penalties for bribery and a focus on transparency, the effectiveness of these measures is undermined by a lack of whistleblower protection and a judiciary that is susceptible to political influence.

In terms of criminal markets, Russia is a significant hub for human trafficking, arms trafficking, and cybercrime, with organized crime networks operating with considerable impunity. The concentration of power in the hands of the government, coupled with widespread corruption and limited civil society engagement, hampers resilience to crime and complicates efforts to address these pervasive issues effectively.

Economy

The economy of the Russian Federation is characterized by a complex investment climate that poses significant challenges for foreign investors. Despite being ranked 28th out of 190 economies in the World Bank’s Doing Business 2020 Report, Russia's governance issues, including a biased judicial system and high levels of corruption, continue to deter foreign direct investment. Additionally, ongoing sanctions from the EU and U.S., coupled with restrictive policies favoring local producers, further complicate the investment landscape, making it essential for U.S. investors to navigate a myriad of regulatory and compliance challenges while ensuring adherence to international sanctions.

Subscribe to

Professional Plus

- Unlimited Access to full Risk Reports

- Full Dataset Download

- API Access

- Virtual Asset Risk Assessments