United States Country Summary

Medium-Low Risk

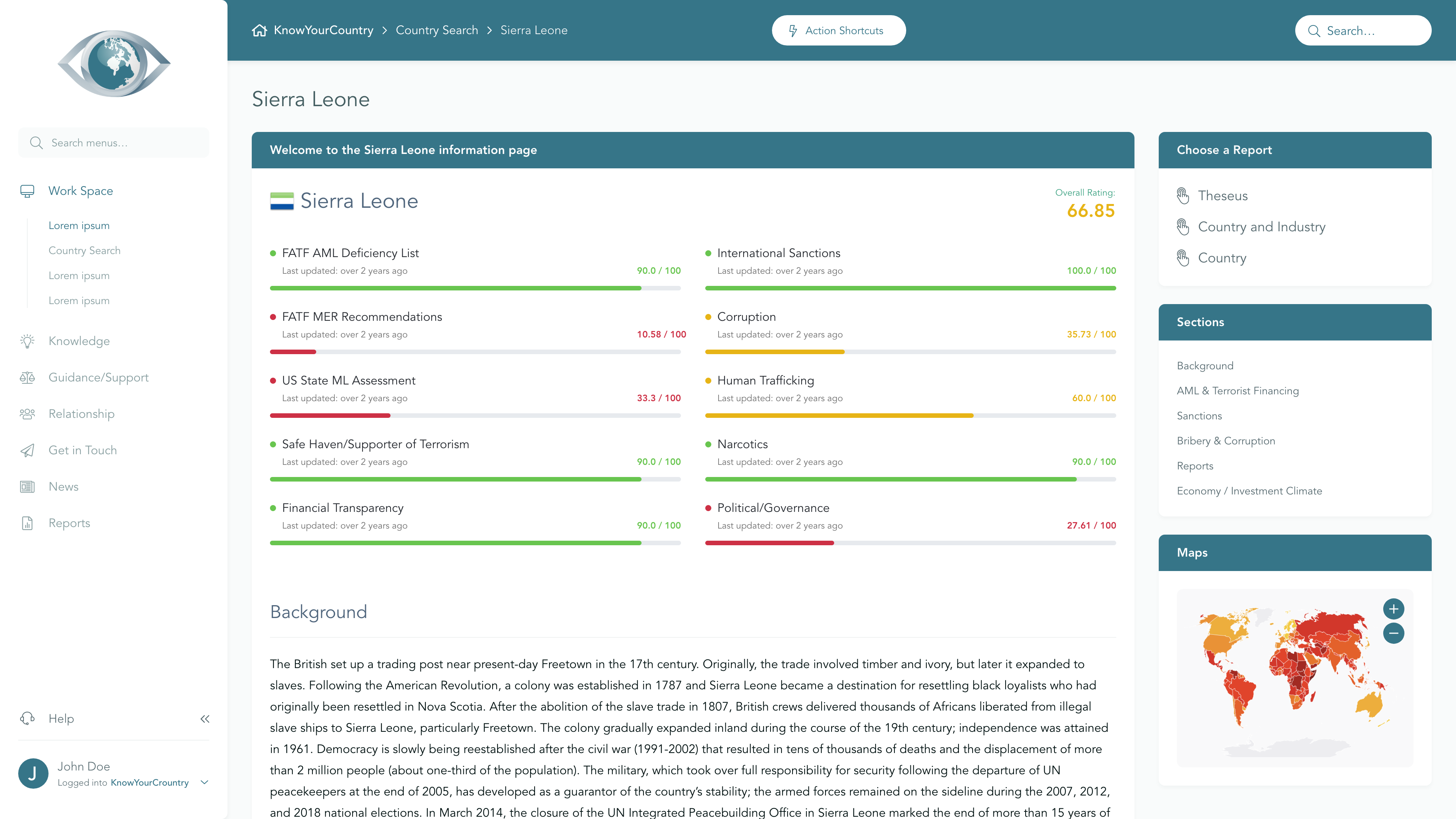

View full Ratings TableSanctions

Lower Concern

FATF AML Deficient List

Lower Concern

Terrorism

Lower Concern

Corruption

Lower Concern

US State ML Assessment

Higher Concern

Criminal Markets (GI Index)

Medium Concern

EU Tax Blacklist

Lower Concern

Offshore Finance Center

Lower Concern

Please note that although the below Summary will give a general outline of the AML risks associated with the jurisdiction, if you are a Regulated entity then you may need to demonstrate that your Jurisdictional AML risk assessment has included a full assessment of the risk elements that have been identified as underpinning overall Country AML risk. To satisfy these requirements, we would recommend that you use our Subscription area.

If you would like a demo of our Subscription area, please reserve a day/time that suits you best using this link, or you may Contact Us for further information.

Anti Money Laundering

FATF Status

The United States is not on the FATF List of Countries that have been identified as having strategic AML deficiencies

Compliance with FATF Recommendations

The latest follow-up Mutual Evaluation Report relating to the implementation of anti-money laundering and counter-terrorist financing standards in the USA was undertaken by in 2024. According to that Evaluation, the USA was deemed Compliant for 9 and Largely Compliant for 23 of the FATF 40 Recommendations. It remains Highly Effective for 4 and Substantially Effective for 4 with regard to the 11 areas of Effectiveness of its AML/CFT Regime.

Sanctions

There are currently no international sanctions in force against United States.

Criminality

Rating |

0 (bad) - 100 (good) |

|---|---|

| Transparency International Corruption Index | 64 |

| World Bank: Control of Corruption Percentile Rank | 83 |

The United States faces significant challenges related to crime and corruption, particularly in areas such as human trafficking, drug trade, and cyber crimes, with various criminal networks exerting influence across the country. Despite these issues, the US demonstrates resilience through a robust legal framework, international cooperation efforts, and active civil society engagement aimed at supporting victims and enhancing public trust in governance.

Economy

The United States boasts the largest economy in the world, with a nominal GDP exceeding $29 trillion in 2024, representing over 25% of global economic output. Its economy is primarily consumer-driven, with personal consumption expenditures surpassing $18.5 trillion in 2023, although it grapples with significant income inequality and poverty among millions. The investment climate remains strong, bolstered by a robust legal framework, a large consumer market, and a skilled workforce, despite challenges such as regulatory complexities and high corporate tax rates that may deter some investors.

Subscribe to

Professional Plus

- Unlimited Access to full Risk Reports

- Full Dataset Download

- API Access

- Virtual Asset Risk Assessments